No one could have anticipated how quickly events would unfold. It kicked off on a positive footing with a strengthening labour market and a growing global economy – gradually rebounding from the pandemic. It was then abruptly punctuated as geopolitical events took hold and dominated the rest of the year. In fact, the editors of the Collins Dictionary declared ‘permacrisis’ to be their 2022 word of the year. Permacrisis is defined as ‘an extended period of instability and insecurity, especially one resulting from a series of catastrophic events.’ That just about sums it up!

The Invasion and its impact • The Russian invasion of Ukraine at the end of February was the prime ‘permacrisis’ catalyst, which as well as being a humanitarian disaster, forced global energy and other commodity prices higher, intensifying the already heightened inflationary backdrop. The economic impact was, and continues to be, felt around the globe. In early spring, the outlook for macroeconomic policy quickly became critical. The path of the global economy was primarily shaped by the consequences of Russia’s invasion, major central

banks’ policies and their ability to keep inflation expectations anchored, while allowing a supportive environment for growth –

a challenging balance to strike.

Slowing Growth - A continuing theme • Even before the invasion, the mix of uncertainties led the International Monetary Fund (IMF) to downgrade its global growth forecast for 2022 when its economic musings were released last January. While the international soothsayer outlined expectations for the global recovery to continue in 2022, it predicted a ‘disrupted recovery’ with growth forecast to moderate.

• Back in January, the Organisation for Economic Co-operation and Development (OECD) expected growth to moderate to 4.4% in 2022. This reflected forecast markdowns in the US and China – a theme which continued throughout the year, as growth faltered in the world’s two largest economies.

Inflation and Interest Rates - An ongoing battle • Inflation exceeded all forecasts in 2022, reaching 11% in the eurozone and UK, and around 8% in the US. The Federal Reserve, European Central Bank (ECB) and Bank of England (BoE) raised interest rates in outsized moves in the year in an attempt to temper inflation. On home shores, since December 2021, the BoE increased Bank Rate from 0.1% to 3.5%. The impact of monetary tightening on the economy is visible, with broader effects on consumer demand, spending, the housing market and job markets.

Closer to home - all change on the political front • As 2022 progressed, political events dominated the domestic landscape. The year saw three Prime Ministers, four Chancellors and a whole series of fiscal events. In September, the fallout from former Chancellor Kwasi Kwarteng’s controversial Growth Plan sent shockwaves through financial markets, causing significant moves in government bond prices and yields, a hit on sterling and chaos on the mortgage market. The BoE sought to intervene with a short-term bond buying programme, while the IMF

weighed in with concerns of its own. Following new Chancellor Jeremy Hunt’s reversal of most of the mini-Budget measures, a level of stability resumed. Challenges with household finances were somewhat supported by the Energy Price Guarantee, one measure which was retained.

• The Autumn Statement in November brought a swathe of announcements set to pull people into paying higher rates of Income Tax, with more people paying Inheritance Tax (IHT), a cut to tax-free income from dividends and a reduction in Capital

Gains Tax (CGT) allowances. The Edinburgh Reforms announced in early December look set to shake up financial service regulation in

the coming year. As the year closes amid widespread industrial action, Prime Minister Rishi Sunak faces a multitude of challenges as we head into the new year, including winning electoral favour for his party.

Volatility - A known known? • The year was a challenging one for global stock markets. All major indices had a tough time as soaring inflation, rising interest rates and the Ukraine invasion critically entwined to host a potentially disconcerting backdrop for investors. Markets experienced significant volatility and extended downturns throughout the year. Global stock markets have had some positive periods, and as the year closes out, some momentum has returned.

• The CBOE Volatility Index or The VIX® Index is a measure of the US stock market’s expectation of volatility based on S&P 500 index options. Widely known as the ‘Fear Index,’ the higher The VIX® Index, the greater the level of fear and uncertainty in the market, with levels above 30 indicating tremendous uncertainty. The VIX® Index topped 36 in early March as the Russian invasion impacted; it subsequently fluctuated throughout 2022 between 18 and 34, moderating in the low / mid 20s at the end of the year.

• In early December, The VIX® Index dropped below the key 20 threshold, reaching its lowest level in more than three months as Wall Street grew increasingly bullish about the stock market’s future prospects. The VIX® Index reached a record high of 82.69000 in March 2020 at the outset of the pandemic and a record low of 9.14000 in November 2017.

Bulls and bears – a sense of perspective • Although 2022 was a year littered with geopolitical events and market shocks, it’s useful to put what happened into wider historical context. The frequency of market shocks has increased and, to a certain degree, intensified over the past few years. Recent catalysts such as the Brexit vote, the election of Trump as US President, the pandemic and subsequent lockdowns, the Ukraine invasion and the UK political landscape in 2022, all triggered investment volatility. Interestingly, 2022 has been different because those exposed to lower risk assets such as bonds were adversely impacted. With rising inflation, higher exposure to fixed income strategies, including UK government bonds, bond yields rose and bond prices fell, which had a detrimental impact on their

performance. This was further exacerbated by the political turmoil in the autumn, in particular the unfunded tax pledges in the mini-Budget. Reversal of the measures and return of political stability led investment markets to recover some losses.

• The 2022 bear market differs because with crisis-fuelled bear markets, such as the pandemic-driven 2020 crash, a gradual easing of monetary policy was the antidote. This time, however, policy tightening will likely be the cause of economic slowing, as central bankers grapple with inflation. As an individual investor, the key to approaching any turbulence is to understand that market swings are normal and relatively insignificant over the long-term.

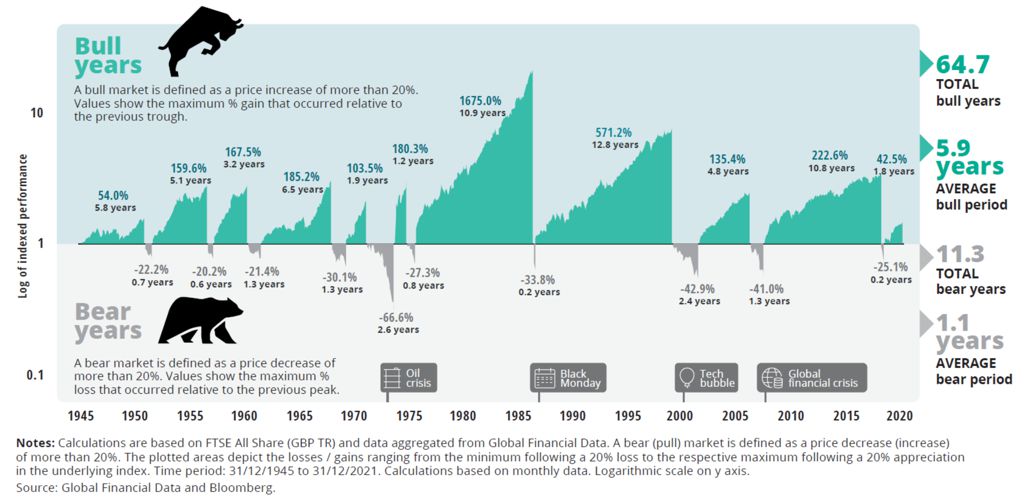

• This chart about bull and bear runs through the years shows that over a 75-year period to 2020, there were 64.7 bull years (the average bull period was 5.9 years), and 11.3 bear years in total (the average bear period was 1.1 years). Historically, bull markets have beaten bears and driven long-term gains. Investing for the long-term and having a disciplined, well constructed plan can help you reach your goals. Also, opportunities do arise in depressed market conditions, like the ability to purchase quality stocks effectively at a discount.

Looking ahead – recession and recovery • As 2023 dawns, we enter the new year under the spectre of potential recessions in developed markets, with high inflation and interest rates continuing to place downward pressure on growth. Predictions can be troublesome; after all, at the turn of 2022; who would have called doubledigit inflation in the West, the most aggressive US monetary policy tightening for decades, a crash in government bonds and war in Europe?

• What we do know though is that providing our clients with a sound strategy and a financial plan able to flex

with changing needs, which is positioned for the long-term and broadly diversified across a range of global assets, will help bring resilience in different market conditions. It’s important to remember that market volatility is normal, and history shows that those who are patient and stick to their plans are more likely to achieve their financial objectives. Rebalancing your portfolio will ensure your asset allocation remains aligned with your objectives.

While we aren’t in the habit of making predictions for the year ahead, here are a selection from some reputable banks, organisations and asset managers for you to ponder:

- The BoE expects inflation to fall sharply from the middle of 2023

- The OECD forecasts a ‘significant growth slowdown’ globally in 2023, with tighter monetary policy, persistently high energy prices, weak real household income growth and declining confidence all weighing on growth

- The Confederation of British Industry (CBI) projects that the UK economy is on course to shrink by 0.4% in 2023, as persistently high inflation continues to dampen longer-term growth prospects, with unemployment expected to peak at 5.0% in late 2023 and early 2024, up from 3.6% currently, while gross domestic product (GDP) is forecast to return to its pre-pandemic level in mid-2024.

- Recessions are anticipated in the eurozone and UK starting in late 2022 and in the US in Q2 and Q3 – Fitch Ratings

- Despite the headwinds to growth, JP Morgan sees the potential for stronger markets in 2023, ‘a dramatic reset in valuations has created one of the most attractive entry points for both stocks and bonds in over a decade’.

- Mike Wilson, Chief Investment Officer and Chief US Equity Strategist at Morgan Stanley, believes, “Because we are closer to the end of the cycle at this point, trends for these key variables can zig and zag before the final path is clear. While flexibility is

always important to successful investing, it’s critical now”.

- Real estate company CBRE expect a moderate UK recession throughout 2023 and in 2024, ‘the economy will recover, growing by 1.7%. The economy appears sufficiently healthy to avoid long-term scarring, such as reduced business investment, high long-run unemployment, and permanent decline in key sectors. As inflation reduces and the Bank decreases interest rates, consumers’ incomes will restore their purchasing power. Spending will increase, ushering growth in output in early 2024, with strong recovery underway by the second half of 2024.’

The value of investments can go down as well as up and you may not get back the full amount you invested.

The past is not a guide to future performance and past performance may not necessarily be repeated.

It is important to take professional advice before making any decision relating to your personal finances.

This document does not provide individual tailored investment advice and is for guidance only.

Our service is driven by our fantastic team. Here you will find all our staff - we think it's important for our clients to build close relationships with us...

Send us a message - Please use the form below to contact us, we will reply as soon as we can. Alternatively you can call us on Tel. (+44) 0115 972 7666.