UK economic growth forecast upgraded - An updated forecast published last month by the Organisation for Economic Co-operation and Development

(OECD) suggests the UK will be the joint-second fastest growing economy among the G7 nations this year.

• According to the OECD’s latest projections, the UK economy is

set to expand by 1.1% across the whole of 2024, a significant

upgrade from the think tank’s previous estimate of 0.4% which

was released in May. The new forecast places the UK alongside

Canada and France in the G7 rankings, with only the US economy

forecast to grow more strongly this year.

• Gross domestic product (GDP) statistics released last month by

the Office for National Statistics (ONS), however, did show that

the UK economy unexpectedly failed to grow during July, after

also flatlining in June. Despite the lack of growth across both

of these months, ONS did note that ‘longer term strength in the

services sector’ had resulted in some growth across the economy

during the three months to July as a whole.

• Data from the latest S&P Global/CIPS UK Purchasing Managers’

Index (PMI) also suggests growth across the UK private sector

has softened more recently, with its preliminary headline

indicator standing at 52.9 in September, down from August’s

figure of 53.8. This does, however, mean that for the eleventh

consecutive month, the Index remained above the 50 threshold

that denotes expansion in private sector output.

• Commenting on the findings, S&P Global Market Intelligence’s

Chief Business Economist Chris Williamson acknowledged that

the latest data did suggest output growth in both manufacturing

and services had moderated last month. He added, “A slight

cooling of output growth across manufacturing and services in

September should not be seen as too concerning, as the survey data

are still consistent with the economy growing at a rate approaching

0.3% in the third quarter.”

Interest rates set to gradually head lower - While last month did see the Bank of England (BoE) maintain

interest rates at their current level of 5%, the Bank’s Governor Andrew Bailey also stated his optimism that rates

are now on a downward path.

At its latest meeting, which concluded on 18 September, the

BoE’s Monetary Policy Committee (MPC) voted by an 8–1 majority

to leave Bank Rate on hold. The one dissenting voice voted

for what would have been a second successive quarter-point

cut following the committee’s decision to reduce rates in early

August, the first reduction since 2020.

The minutes to the meeting, however, did strike a fairly cautious

note. They stated that the decision to hold rates was ‘guided

by the need to squeeze persistent inflationary pressures’ out of

the economy and that monetary policy would need to ‘remain

restrictive’ until the risks to inflation have ‘dissipated further.’

On the same day the MPC meeting ended, ONS published the

latest inflation data, which revealed that August’s headline annual

rate was unchanged at 2.2%. Although this did mean the rate

therefore remained marginally ahead of the BoE’s 2% target

level, the figure was exactly in line with analysts’ expectations.

Speaking a few days after the inflation figures were released, the

BoE Governor said he was “very encouraged” by the downward

path of inflation over the past two years and that the Bank

should be able to reduce rates as it becomes more confident

inflation will remain close to target. Mr Bailey concluded, “I do

think the path for interest rates will be downwards, gradually.”

A Reuters poll released last month also revealed that most

economists expect one more rate cut this year, with a large

majority predicting the BoE will sanction a reduction after the

MPC’s next meeting, which is scheduled for 7 November.

Markets • An escalation of the conflict in the Middle East weighed

on markets at the end of September, with investors and

traders closely monitoring developments in the region.

• At month end, stocks retreated following implications from

Federal Reserve Chairman Jerome Powell that further interest

rate cuts are likely to occur at a more measured pace.

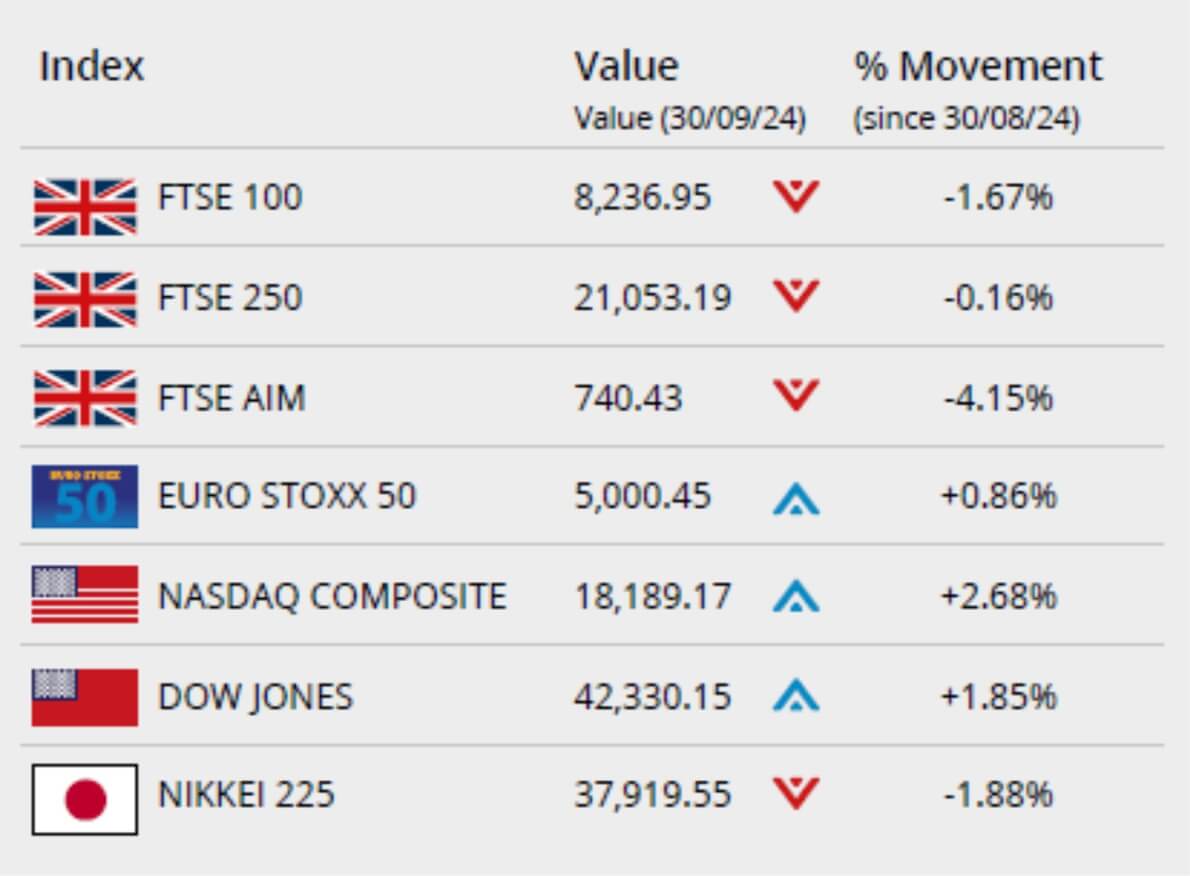

• Across the pond, the Dow Jones closed the month up 1.85%

on 42,330.15. The tech-orientated NASDAQ closed the month

up 2.68% on 18,189.17.

• On home shores, the FTSE 100 index closed the month on

8,236.95, a loss of 1.67%, while the FTSE 250 closed the

month 0.16% lower on 21,053.19. The FTSE AIM closed on

740.43, a loss of 4.15% in the month. The Euro Stoxx 50

closed the month on 5,000.45, up 0.86%. In Japan, the Nikkei

225 closed September on 37,919.55, a monthly loss of 1.88%.

• On the foreign exchanges, the euro closed the month at €1.20

against sterling. The US dollar closed at $1.33 against sterling

and at $1.11 against the euro.

• Brent crude closed September trading at $71.65 a barrel,

a loss over the month of 6.74%. The conflict in the Middle

East is causing some price volatility. OPEC+ plans to begin

increasing production in December is pressurising prices, while weak demand in China also weighs. Gold closed the

month trading at $2,629.95 a troy ounce, a monthly gain of

4.64%. Prices retreated at month end, reversing recent strong

gains as increased safe-haven demand prompted a rally in the

precious metal.

Retail sales stronger than expected

The latest official retail sales statistics revealed a healthy

growth in sales volumes during August, while more recent

survey data points to further modest improvement both last

month and in October.

Figures released by ONS showed that total retail sales volumes

rose by 1.0% in August, following upwardly revised monthly

growth of 0.7% in July. ONS reported that August’s rise, which

was higher than economists had predicted, was boosted by

warmer weather and end-of-season sales.

Evidence from last month’s CBI Distributive Trades Survey also

suggests retailers expect the summer sales improvement to

have continued into the autumn period, with its annual retail

sales gauge rising to +4 in September from -27 in August. In

addition, retailers’ expectations for sales in the month ahead

(October) rose to +5; this represents the strongest response to

this question since April 2023.

CBI Principal Economist Martin Sartorius said retailers would

“welcome” the modest sales growth reported in the latest survey.

He also added a note of caution saying, “While some firms within

the retail sector are beginning to see tailwinds from rising household

incomes, others report that consumer spending habits are still being

affected by the increase in prices over the last few years.”

National debt looks set to soar • Analysis published last month by the Office for Budget

Responsibility (OBR) suggests national debt could triple over

the coming decades if future governments take no action.

• In its latest Fiscal Risks and Sustainability Report, the OBR said

debt is currently on course to rise from almost 100% of annual

GDP to 274% of GDP over the next 50 years due to pressures

including an ageing population, climate change and geopolitical

risks. It also warned that, without any change in policy or a

return to post-war productivity levels, the public finances

were unsustainable over the long term, and that ‘something's

got to give.’

• The OBR is also tasked with producing a more detailed

five-year outlook for the country’s finances that will be

published alongside Chancellor Rachel Reeves’ first Budget,

due to be delivered on 30 October. The Chancellor has

previously warned the Budget will involve “difficult decisions”

on tax, spending and welfare.

• Data released last month by ONS showed that government

borrowing in August totalled £13.7bn, the highest figure for that

month since 2021. This took borrowing in the first five months of

the financial year to £64.1bn, £6bn higher than the OBR forecast

at the last Budget.

The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated.

Our service is driven by our fantastic team. Here you will find all our staff - we think it's important for our clients to build close relationships with us...

Send us a message - Please use the form below to contact us, we will reply as soon as we can. Alternatively you can call us on Tel. (+44) 0115 972 7666.

• According to the OECD’s latest projections, the UK economy is

set to expand by 1.1% across the whole of 2024, a significant

upgrade from the think tank’s previous estimate of 0.4% which

was released in May. The new forecast places the UK alongside

Canada and France in the G7 rankings, with only the US economy

forecast to grow more strongly this year.

• According to the OECD’s latest projections, the UK economy is

set to expand by 1.1% across the whole of 2024, a significant

upgrade from the think tank’s previous estimate of 0.4% which

was released in May. The new forecast places the UK alongside

Canada and France in the G7 rankings, with only the US economy

forecast to grow more strongly this year.

Interest rates set to gradually head lower - While last month did see the Bank of England (BoE) maintain

interest rates at their current level of 5%, the Bank’s Governor Andrew Bailey also stated his optimism that rates

are now on a downward path.

Interest rates set to gradually head lower - While last month did see the Bank of England (BoE) maintain

interest rates at their current level of 5%, the Bank’s Governor Andrew Bailey also stated his optimism that rates

are now on a downward path.

National debt looks set to soar

National debt looks set to soar